NIIT – Business Analysis

— November 9, 2013First, the Business

The education industry in India is benefiting from rising industry demand as well as a growing population and sub-par education system. The opportunity in this sector is, therefore, exciting. However, the training industry is mature and competitive.

NIIT is one of India’s leading players in the vocational training industry with a global presence. It’s the third largest education provider (after CORE Education and EduComp) by sales turnover and Individuals, Enterprises, Schools and Colleges are its key customers.

As per FY12 annual report, NIIT had

- Presence in 40 countries worldwide

- Impacted over 35 million learners since inception

- Served 17,000 schools

- One of the largest learning content development facilities in the world

In order to understand NIIT’s business, it’s important for us to understand the vocational training market in India.

The education ecosystem in India has two major categories:

- Vocational/IT training

- Education Solutions & Services (Software solutions and services to supplement education in schools, colleges and other educational intuitions) .

NIIT is a leading player in the vocational/IT training market. CORE Education and EduComp Solutions are leading players in the Education Solutions market.

Vocational training prepares students and professionals for specific trades, crafts and careers. In India, vocational training is closely coupled with the IT,Banking & Finance, Knowledge Process Outsourcing (KPO) and Business Process Management (BPM) industries, as they are the key job creators in the knowledge economy.

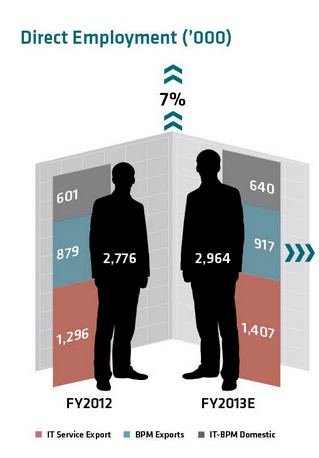

The chart below is the Direct Employment Opportunities / Jobs in ITES sector in India for the years FY 2012 and FY 2013 as per nasscom.com

picture reference – http://www.nasscom.in/knowledge-professionals

Vocational training with live coaching is a capital-intensive business and most of the companies involved in this market including NIIT have adopted a franchise model.

A franchise typically involves the granting by one party (a franchisor) to another party (a franchisee) the right to carry on a particular name or trade mark, according to an identified system, usually within a territory or at a location, for an agreed upon term. The franchisee is granted a franchise license to use the franchisor’s trademarks, systems, signage, software, and other proprietary tools and systems in accordance with the guidelines in the franchise contract. The franchise contract requires the franchise to run the business according to the operations manual and also pay an upfront franchise fee (license fee), and ongoing royalties.” ( reference wikipedia )

Rajendra Pawar, the co-founder and chairman of NIIT started NIIT based on an idea that everybody told him would never work, flirted with financial ruin, and then came up with an ingenious franchise model.

Mr. Pawar says franchising was a way to grow a business rapidly. After months of pondering, he came up with a uniquely Indian twist on the model. He would try to get the most respected families in small communities to sign up as his franchisees. Indians put great emphasis on the concept of pride and respect (izzat). To lose izzat is to lose everything. Pawar figured out that if he could get respected families to be franchisees they’d have powerful incentive to manage the schools well, protecting their Izzat- along with NIIT brand name. His model was a success and NIIT franchisees have spread NIIT everywhere from China to Ghana to Russia.

( Source : http://www.slideshare.net/finlifecon63/franchise-managemnt-presentation )

NIIT’s Franchise Model – How it works

The franchisees pay for marketing and infrastructure- space, desks, and computers, NIIT provides all the course materials and selects and trains all the faculty members. In return, the company gets royalties of roughly 20 percent on student tuitions and also reimbursed for the teaching materials it supplies. Some of the highlights of NIIT’s franchise model below:

- Equips Franchisee with cutting-edge curriculum, courseware, detailed operation manuals and process that make it a preferred choice of individuals and enterprises. NIIT has the second largest library of courseware in the world, for IT and Management studies

- With an umbrella of a highly reputed and credible brand names and an alumni base of 5 million students worldwide, NIIT is a household name in India and a leading global IT education provider

- NIIT allows Franchisees to grow by providing them with the facility of multiple education centers and a wide array of products

There are other companies in the vocational training market like “Aptech Ltd” and LCC ( Lakhotia computer center ), which have also adopted the franchise model.

Risks (what can go wrong)

The education Industry is undergoing a transformation / disruption due to technology, similar to the publishing and music industries.To understand the competitive structure of the industry in which NIIT operates, we can use “Porter’s 5 Forces”. (“Michael E. Porter, who is a leading authority on competitive strategy popularized Porter’s 5 Forces”)

#1 Threat of New Entrants

The barrier to enter the IT/vocational training business is not very high, which is evident from the high number of big and small companies engaged in this industry.

Economies of Scale

The resource intensive nature of IT/vocational training (especially in-class / live coaching) makes it hard to lower the cost per unit produced. As a result it’s difficult for NIIT or any company in this industry to create a barrier to entry based on economies of scale.

Customer Switching Cost

There are no fixed costs for the customers of NIIT if they decide to change providers. There are ways in which individual customers / students can be locked in for extended periods of time by various certificate programs but they are not applicable to institutional or enterprise customers. As per FY 2013 , 41% of NIIT’s revenue are from corporations and institutions and 51% from individuals.

#2 Bargaining Power of the Buyer

The Big Institutional and Enterprise customers of NIIT have the bargaining power and can extract more value from the services offered by NIIT at a lesser price due to the following.

Fewer Buyers: There are relatively less Enterprise customers and they purchase in large volumes; hence they have an advantage in negotiating price and terms of service

No Differentiation: Training is an important aspect for individuals and institutions; however, unlike software, training is not sticky. An institution or individual can choose to change the provider at any point as there are many companies offering similar training packages to those that NIIT provides.

The bargaining power of NIIT’s buyers is evident from the significantly higher “Days Sales Outstanding” DSO of 138.07 days compared to it’s peers and industry average.

“Days Sales Outstanding (DSO) is a measure of the average number of days that a company takes to collect revenue after a sale has been made. A low DSO number means that it takes a company fewer days to collect its accounts receivable. A high DSO number shows that a company is selling its product to customers on credit and taking longer to collect money.”. (source : http://www.investopedia.com/ )

#3 Bargaining Power of Suppliers

NIIT’s suppliers include, hardware and software suppliers, courseware material providers, Marketing agencies, Office supplies, property managers/landlords and human resource contractors. We can understand the bargaining power of NIIT’s suppliers by looking at the “payable period”.

As per Investopedia “Payable Period” is the average period that a company has between receiving goods and paying its suppliers for the goods, utilizing accounts payable and cost of sales values. The value is generally determined either quarterly or yearly, thereby substituting for N either 90 (for quarterly values) or 365 (for yearly values).

The greater the number of days the company has to pay its suppliers, the more cash the company will have to direct to other working capital needs. This provides an indication of how long the company typically takes to pay its suppliers or creditors. Payable periods is also a clue to understand the bargaining power of a company’s suppliers. Higher the “Payable period” lower the bargaining power of the suppliers.

(source : http://www.investopedia.com/ )

NIIT has an average “payable period” of 176 days over past 5 years compared to it’s peer Aptech had an average “payable period” of 168 days during the same period.

#4 Threat of substitutes

A substitute product performs a similar function as the original product. Video conferencing is a substitute for travel. Email is a substitute for physical mail. When the threat of substitutes is high, the industry as a whole will not be profitable. (reference janav.wordpress.com )

The education industry is in the midst of a technological revolution helping democratize the delivery of content. There are many companies, non-profit’s and universities contributing to this phenomenon. The result is lowering of cost educational content delivered on scale.

NIIT also faces eroding market share in corporate training and services due to emphasis on in-house training in many of the big IT services companies in India. Infosys for example has developed a campus in Mysore,Karnataka dedicated for in-house training employing full-time educators.

NIIT has reacted to this threat by focusing on their cloud initiative. In conclusion, It’s hard to compete with “Free” or “Freemium” business models. Some of the Substitutes are listed below

Universities Offering their courses (including IT ) for free online

- MIT – OpenCourseware – FREE (http://ocw.mit.edu/index.htm )

- Stanford Online – FREE ( http://online.stanford.edu/courses )

Non-Profits

- Coursera.com – free online classes from 80+ top universities and organizations – FREE

- Udacity.com – Free and affordable classes that anyone can take, anytime

- Khan Academy – Library of over 3000 videos covering everything from arithmetic to physics, finance, IT and history and hundreds of skills to practice – FREE ( https://www.khanacademy.org/ )

Education Platforms / Companies

- Udemy.com – Udemy is an online learning platform (website) that allows instructors to host courses. It’s the iTune for education. – Affordable Prices

- Teamtreehouse.com/ – Technology/IT focused online training with an affordable monthly subscription – Monthly subscription / Affordable Prices

- Lynda.com – IT/Technology focused online education portal focusing on enterprise & institutional customers. – Premium Prices

#5 Rivalry among existing competitors

There are many competitors in the training industry andthere is little service differentiation among the companies in this industry, hence the competition on price is very intense.

The startup cost of a training company is relatively low, especially for smaller concerns that focus on a limited geographic area. Anecdotally I know few training companies / institutions that are run by entrepreneurs who are targeting NIIT’s market and successfully gaining market share.

MasterMind (http://mastermind.bz/) and SATG Software (http://www.stagsoftware.com/) are examples of small to medium size companies focusing on a niche. Both of them are located in Bangalore and cater to the needs of companies in the Silicon Valley of India. These companies were founded by professionals who have years of experience and deep connections in the IT industry.

Mastermind focuses on System administration and IT support. They have instructors who are working professionals and have years of experience in the field. They also recruit some of their students to their IT services group.

SATG Software has a business model that is similar to Mastermind’s, but at a much larger scale. They focus on Semiconductors, Hardware, Firmware and Quality Assurance. They provide both training and placement.

Valuation

Sales Growth

The competitive forces described in the previous section along with the slowdown in IT sector and maturation of the IT/vocational market is reflected in the NIIT’s negative sales growth of -0.93% in the last 3 years and -7.13% in the last 5 years.

Capital Management

| 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | |

| Equity Share Capital | 19.76 | 32.94 | 33.0 | 33.02 | 33.02 | 33.02 |

| Debt/Equity | 0.86 | 0.51 | 0.73 | 0.80 | 0.65 | 0.13 |

| Current Ratio | 1.41 | 1.27 | 1.25 | 1.52 | 1.36 | 1.53 |

| Working Capital | 138.84 | 121.74 | 121.93 | 247.11 | 219.01 | 311.05 |

- NIIT has been maintaining a healthy dividend payout of 33.95%

- NIIT has maintained a consistent current ratio greater than 1, with an average of 1.39 in the past 6 years.

- NIIT had cash and bank balances of Rs 105.8 Cr. at the end of March 31st 2013.

- NIIT has a Contingent liabilities of Rs.164.46 Cr

Capital Efficiency:

NIIT’s average return on capital employed for the last 3 years is 6.29%, significantly lower than its peers in the industry. The average return on capital of its peers like Apetch Ltd. during the same period was 27.38%.The average ROE for the past 5 years is 13.62%. During the same period NIIT’s peer Aptech Ltd. had an average ROE of 16.10%.

Why is Return on Equity important ?

Warren Buffett, Chairman and CEO of Berkshire Hathaway describes the importance of return on equity on shareholder return…

“Just as a 10% return on a business is, all other things being equal, better than a 5% return, so too with corporate rates of returns on equity. Also, a higher return on equity means that surplus funds can be invested to improve business operations without the owners of the business (stockholders) having to invest more capital. It also means that there is less need to borrow.”

To put things in perspective, wide moat business like Coke and IBM had an average ROE of 31.07% and 71.3% respectively in the past 5 years.

Management Profile:

NIIT’s Chief Executive Officer Mr. Vijay Thandani along with Chairman Rajendra S Pawar co-founded NIIT and have grown the company from a single training center in 1982 to a multinational corporation operating in more than 40 countries. As of FY12, promoters hold 33.6% of the company stocks.

Management’s salaries

During FY12, the Chief Executive Officer was paid gross remuneration of Rs 0.96 Cr. This is around 0.87% of the company’s net profit and thus not a big figure.

Substantial equity dilution in the past

NIIT had seen a 66.7% increase in its outstanding equity shares in the year 2007-2008. This was on account of increase in paid-up capital of the Company from Rs. 197,552,060 to Rs. 329,405,726 due to corporate benefits/allotment of Equity Shares such as bonus shares, FCCB conversion and ESOP allotment.

Capital Allocation

With an average return on equity of 13% for the past five years and equally unimpressive return on employed capital compared to its peers and industry average, it’s hard to support the case for NIIT’s efficient capital allocation.

Owner’s Earnings

I will refrain from valuation of the business ( i.e. estimate the fair value of NIIT ) as there are many forces acting on the business of NIIT, hence It’s hard to predict the future of NIIT’s business with certainty.

Instead, I will try to evaluate how the market is valuing NIIT based on “Owners Earnings” made popular by none other than Warren Buffett in his 1986 letter to shareholders

“If we think through these questions, we can gain some insights about what may be called “owner earnings.” These represent (a) reported earnings plus (b) depreciation, depletion, amortization, and certain other non-cash charges such as Company N’s items (1) and (4) less ( c) the average annual amount of capitalized expenditures for plant and equipment, etc. that the business requires to fully maintain its long-term competitive position and its unit volume. (If the business requires additional working capital to maintain its competitive position and unit volume, the increment also should be included in ( c) . However, businesses following the LIFO inventory method usually do not require additional working capital if unit volume does not change.)” – 1986 Berkshire letter

NIIT’s Owner’s Earnings derived from FY 13 (consolidated) Annual Report.

- Net Income / Net Profit: Rs 26.3 Cr.

- + Depreciation, amortization: Rs 78.40 Cr

- +/- Other non cash charges: (Rs. 1.34 Cr)

- - Maintenance Capital Expenditure: (Rs. 56.3 Cr.

- +/- Changes in Working Capital: (Rs. 3.81 Cr)

Owner Earnings: Rs. 43.25 Cr.

The average owner’s earnings for the past 3 years is Rs. 73.4 Cr. and Rs. 32.23 Cr for the past 5 years.

As Prof. Sanjay Bakshi explains in his BFBV lecture notes, using an answer provided by Warren Buffett to one of the shareholders. The actual returns NIIT earns based on average owner’s earning for the past 3 years and current market cap is 22.9% and returns for the past 5 years is 13.5%

It’s needless to say that assuming NIIT will maintain current level of revenue and profitability in future is unrealistic. The best we can do is applying a margin of safety to our expectations on returns.

Disclaimer: I, Hari Ramachandra, have no position in the company or in any company related to the promoter group. Readers are advised to do their own independent assessment before taking any decision. You can expect some errors or forward-looking statements, so do your own research as well.

About author

Hello I am Hari

I have more than 20 years experience in the information technology (IT) industry. I write about what I’m learning and some of the tips I have picked up along the way.

Leave a reply